Navigating all the different taxes that a small business needs to pay can be a complicated affair, especially if it is your first time owning and managing a company. To help you with it, we’ve collated a (relatively) short guide to the taxes you are expected to pay as a limited company with a single owner/director.

Note: This guide does not cover any of the schemes that help offset the costs of running a small business, such as, but not limited to capital allowances (equals tax depreciation on fixed assets), small business rates relief, interest on recovery loan scheme etc. This guide also does not cover all the possible tax scenarios, which are specific to your circumstances. You should review your tax obligations with your accountant.

Corporation tax

Every limited company needs to pay it. It’s a flat rate, which currently stands at 19%. It’s calculated after salaries, tax relief and other business expenses, but before dividends are paid.

Example:

Total earnings: £100

Salary*: -£50

Business expenses*: -£30

Profit before dividends: £20 (=£100-£50-£30)

Corporate tax: £3.8 (=19% of £20)

Profit after tax (available for dividends or reinvestment): £16.2 (=£20-£3.8)

*Salary is one of the allowable business expenses. To see what qualifies as a business expense, read more here.

To find out how to register to pay Corporation tax (which needs to be done within the first 3 months after you’ve started your trade), you can read our guide here.

Already running a business? Handle money and accept payments in one app.

Taxes related to Director/Owner’s income

Director/Owner related taxes differ from sole trader taxes or employee taxes. When you have your own limited company, the company is the one that pays your salary, but also you are the one to work out how much it should be (or it is calculated by your accountant).

Apart from salary earnings, as a Director and an Owner, you are also entitled to the company's dividends, which is another way to earn money from your business.

Whilst money is money, your salary and your dividend earnings are taxed differently. To reduce the overall tax bill, many business owners, who are also directors, tend to have a combination of low salary and dividends as take-home earnings. The reason for this is that as per HMRC’s guidelines directors are classed as “office holders” and therefore are not subject to National Minimum / Living Wage Regulations. This means that a very low salary (or no salary) can be paid. Reducing Director’s salary amount can help to minimise or avoid Income Tax and/or National Insurance Contributions.

If you are planning to pay yourself as a Director/Owner of a Limited company both salary and dividends, our advice is to always make sure that you separate and categorise these payments. This will help you calculate the required tax rate later on. With GoSolo, you can categorise these payments as: “Director’s wages” and “Dividends” accordingly, as well as make a Note against the transactions if you want to add additional details.

Salary

Salary is one of the allowable business expenses, which means it lowers the amount of Corporation Tax you need to pay (see above on Corporate Tax).

Taxes related to Salary are Income Tax and National Insurance Contributions.

1. Income (Personal) tax

Tax paid on Director’s salary.

Every tax year, there is a tax-free allowance - set at £12,570 for the 2021/22 tax period. If the Director's salary is over the allowance, then the tax rate is calculated based on a specific tax band. The tax band is determined by HMRC based on the total Director’s earnings, which may include dividends, savings interest or capital gains on top of the salary.

2. National Insurance Contributions

Similar to the above, it is another form of tax paid on the Director’s salary but calculated slightly differently from Income Tax. Assuming your company does not have any employees, there are two thresholds to consider:

- The Lower Earnings Limit: £6,240 per year: above this limit you retain your State Pension contribution record.

- The National Insurance Secondary threshold: is £8,840 per year: below this limit, you do not need to pay any employer’s National Insurance Contributions.

Note that if you have employees, you’d need to consider The National Insurance (NI) Primary threshold, which applies to your employees.

If your aim, as a single Director/Owner, is to avoid paying Income Tax and National Insurance Contributions, then your salary should be between £6,240 and £8,840 per annum.

Before deciding on whether to pay less salary, you should also consider what this means to you in terms of maternity benefits, future mortgage/loan offers and payouts covered under permanent health, critical illness, personal accident or similar policies. All of these are dependent on your salary level and may reduce the benefits amount. If you are unsure of what your salary should be, you should discuss it with your accountant.

Both Income tax and National Insurance Contributions are paid using the PAYE (Pay as You Earn) scheme. To get yourself set up, you’d first need to register for PAYE here. If you do not have any tax deductions (statutory sick pay, maternity/paternity leave or others), all you’d need to do is submit a Full Payment Submission (FPS) to HMRC. FPS will include details about your salary, which will in turn notify HMRC of how much you need to be taxed (nothing if your salary is below the thresholds described above). You can submit FPS yourself via one of the free payroll tools found here. Alternatively, your accountant can take over the paperwork and required submissions. Submissions need to be done every time you pay yourself a salary.

Dividends

If your limited company makes a profit after tax (see Corporation tax section above), the remaining amount can be paid out to you, the single owner of your company, as dividends. If there is no profit after tax (i.e. there is no money left after all the subtractions), then it is illegal to pay yourself dividends. Hence it’s advisable to calculate your balance position before you take out the dividends.

Dividend tax

A dividend tax is a tax paid on Owner’s earnings.

There’s an annual tax-free allowance of £2,000 in dividends on top of Personal Tax-Free Allowance in salary, after which the tax rate is calculated depending on the specific earnings band.

To issue the dividends you need to generate and record a dividend voucher, which includes the following information: date, company name, name of the shareholder who’s paid the dividend and the dividend amount (you can download a template here).

Pension

Not a tax per se, but since we are talking about all payments against your earnings, it’s worth considering a pension too. As a single Director/Owner with no other staff employed, you do not fall under the Pension Auto Enrolment government scheme, however, you need to notify The Pensions Regulator that this is the case here. Once you employ someone, the Pension Auto Enrolment exemption will no longer apply. Whilst it is not mandatory, you might still want to enrol in a personal pension scheme. It’s worth knowing that some of the pension contributions made using your limited company can qualify as a tax-deductible business expense.

Available on Web, iOS, and Android.

![]()

![]()

![]()

VAT

VAT, or Value Added Tax, is a consumption tax and is applicable if a company’s rolling annual taxable turnover exceeds the threshold of £85,000 as of 2021.

Most goods and services fall under the remit of VAT and most of these have a rate of 20%. Some exceptions have a rate of 5% or even 0%. To check if your product/service is under a different VAT rate, check the list here.

Note that it can be beneficial to register for VAT, even if a company’s turnover has not reached £85,000. By doing so, you can claim refunds on VAT from any business expenses. However, that still means that VAT needs to be paid by the company. You may need to register for Making Tax Digital (MTD) for VAT.

Business rates

Business rates - read - business version of council tax. These are paid if you are a brick-and-mortar business (you have an office or a shop) or if you use your home for business purposes (exceptions apply). Business rates are paid to the local authority who will calculate the rate and send you a bill. For business rates estimates, see here.

Taxes related to employing people

If you have an employee(s), you are expected to work out their salary and the related taxes (Income tax, National Insurance Contributions) as well as the pension contribution related to the employee(s). As a business owner, you would be processing tax money to HMRC and relevant authorities on employees’ behalf. The easiest way to go about it is to have an accountant work out the rates for you and produce all the required paperwork.

Other taxes

Capital Gains Tax: paid when you sell a business asset for profit such as a company’s shares or the business itself.

Stamp Duty: paid for transactions on the transfer of land, or transactions related to the purchase of shares of other companies.

Next steps

If your main aim is to reduce the amount of time it requires to manage taxes, then:

- Check if VAT, business rates, pension, taxes related to employing employees or any other taxes (Capital Gains Tax, Stamp Duty Tax or others) apply to your business. If none of these apply, proceed as follows.

- Register on PAYE here.

- In the first month of trading, keep your salary to under £785 (but over £535) to be under the National Insurance Secondary threshold - to avoid paying Income tax and National Insurance Contributions. At these salary levels, your state pension is protected.

- Before you pay yourself a salary, submit an FPS via payroll software, confirming that no income tax or National Insurance Contributions are required in this month.

- Once you’ve paid yourself a salary, calculate how much money (profit) remains in the account at the end of the month.

- If there is profit, calculate the amount of Corporation Tax (19% off the remaining balance) that you need to keep in your business bank account for future tax payments.

- After subtracting Corporation Tax, see what remains and decide if you want to pay this money to yourself or spend it on the business (e.g. rent a bigger office or buy additional machinery).

- If you want to pay money to yourself, see if it’s under £2000 cumulatively within the company operating year. If it is, fill out a dividend issue template and transfer the money to your account as a dividend payment.

- Going into next month, review your total earnings, and, if required, adjust your salary and dividends.

- Pay Corporation Tax at the end of your company’s operating year here.

WARNING: There are strict deadlines for registering for VAT, Corporation Tax etc and, if they are not met, penalties are automatically charged. If the returns are submitted late there are also penalties. The penalties can be large.

Helpful tips

- Open a business bank account for your business to keep track of all your business transactions.

- Manage your transactions by categorising them (e.g. “Salary”, “Travel”), leaving notes and attaching receipts against them.

- Keep a clear audit trail of your sales by matching up invoices with your transactions (done automatically with GoSolo business bank account).

- Before transferring money to a personal account, estimate how much tax you would need to pay - this amount should remain in your business bank account for future tax payments.

- If you set up on your own and were filing self-assessment tax returns beforehand you do not need to reregister for self-assessment but you will need to register for Class 2 National Insurance.

- Get a professionally qualified accountant to spend less time managing taxes (message us at we@gosolo.net if you can’t find one and we can provide you with a recommendation).

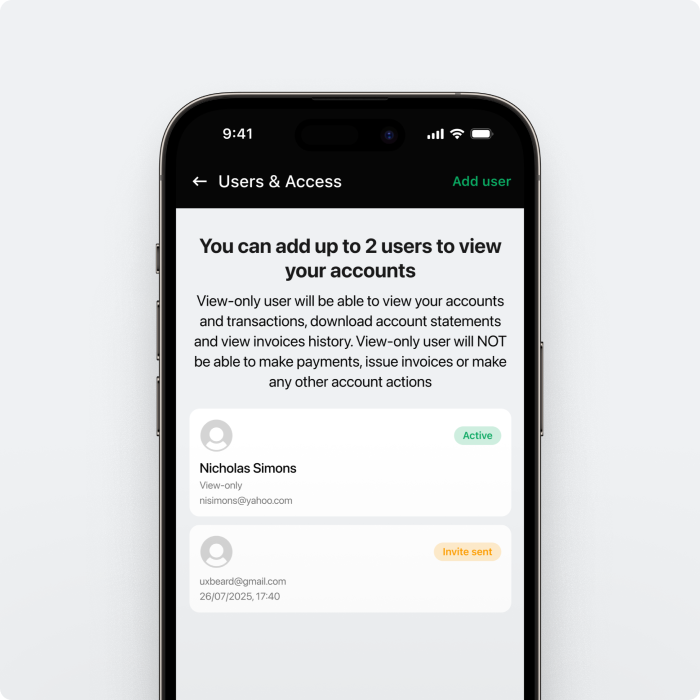

- Share access to your business bank account with your accountant to help them review your transactions - you can add up to 2 view-only users to your GoSolo business bank account.

- With the compulsory introduction of Making Tax Digital for Tax being phased in speak to your accountant about what software packages you should consider.

Final comments

The information contained in this guide is correct and based on our understanding of the law at the date of publication (October 2021). It is intended as an aid and cannot be expected to replace specific professional advice and judgement. No responsibility will be accepted for errors or omissions. It is the responsibility of those using the information to ensure that it meets the law at the time of use.

We hope you found this guide useful and if you are interested in more information, feel free to message us at we@gosolo.net.