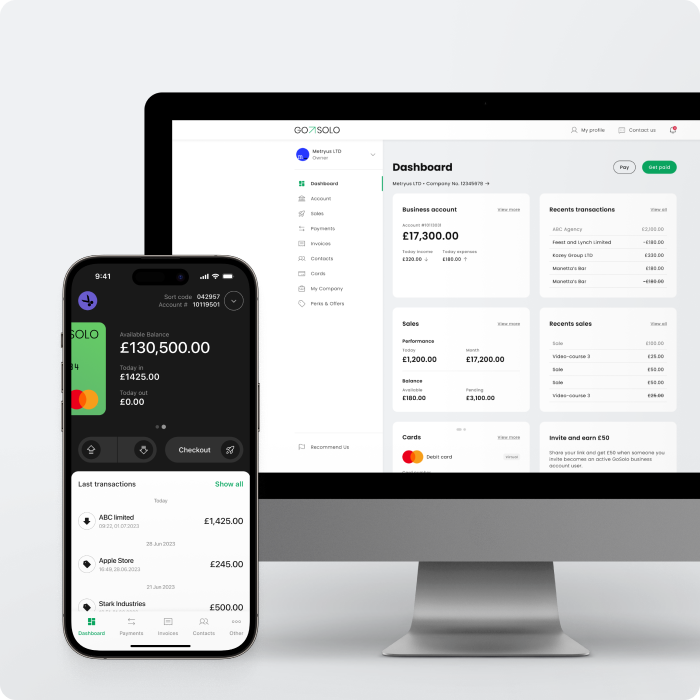

⚡ TL;DR:

- Open-amount payment links—also known as “pay what you want” or “pay what you choose” links—let your customers set the amount they pay at checkout.

- GoSolo offers these links natively (and for free) as part of your business account. No need for Stripe, third-party apps, or extra integrations.

- Most UK business accounts don’t support open-amount payment links, or they charge higher fees per transaction.

- If you’re a freelancer, small business owner, startup, or non-UK resident looking to do business in the UK, GoSolo keeps things transparent, simple, and accessible—so you can focus on growing your venture, not wrestling with payment tools.

What Is an Open-amount (“Pay What You Want”) Payment Link?

Open-amount payment links have transformed how businesses collect payments online—especially in the age of digital wallets, mobile payments, and flexible pricing models. But what exactly are they?

- An open-amount payment link is a shareable checkout link where the payer (customer, client, supporter, etc.) enters the amount they want to pay, instead of being charged a fixed price.

- Also called “pay what you want,” “pay what you choose,” or “open-amount” links, these are ideal for situations where the value isn’t always the same—think tips, donations, deposits, flexible service fees, or custom orders.

- In GoSolo, creating an open-amount payment link is as easy as a few clicks, with no extra software or coding required. It’s built directly into your free business account.

Why is this such a game-changer?

Traditionally, UK business accounts (and most payment providers) only let you request a specific sum—meaning you have to send a new link every time the amount changes. Open-amount links flip the script: you send one link, and your customer decides what to pay based on context, agreement, or generosity.

How To Use Open-Amount Links in the UK

Open-amount payment links aren’t just for quirky tech startups or donation campaigns. They’re practical for almost every type of UK business, especially if you value flexibility, transparency, and customer empowerment.

Who uses them?

- Freelancers & consultants: Charge for time, partial work, or outcome-based projects—no more awkward back-and-forth about custom amounts.

- E-commerce sellers: Collect top-ups, custom orders, or donations alongside fixed-price products.

- Trades & services (builders, cleaners, transport): Take deposits, extras, or partial payments without chasing new invoices.

- Agencies & marketers: Bill for ad spend, flexible retainers, or unplanned extras—let the client pay what’s fair.

- Charities & non-profits: Accept donations of any size, with donors setting their own level of support.

- Delivery drivers & local businesses: Enable tips or variable charges, especially when customer needs can’t be predicted.

Typical scenarios:

- Collecting deposits or part-payments before starting a job.

- Handling top-ups, project scope changes, or extras after a quote.

- Allowing customers to “pay what you choose” for a trial, sample, or digital product.

- Accepting donations or tips with no minimum required.

- Issuing partial refunds or adjustments without creating new invoices each time.

In short: If your business ever needs to collect money where the amount isn’t set in stone, open-amount payment links are your secret weapon.

UK Business Accounts That Offer (or Don’t Offer) Open-amount Payment Links—Costs and Fees

Not all payment link providers are created equal, especially when it comes to open-amount capability, fee transparency, and ease of use. Here’s how leading UK business accounts stack up:

GoSolo

- Open-amount links: Yes—natively supported.

- Pricing: £0/month; Interchange++ (market-leading): actual card cost + 0.5% + 20p.

- Integrations needed: None. Works directly in the GoSolo web and mobile app.

- Reusable links: Yes—generate once, use as often as you like.

- Other features: custom branding, payment tracking and notifications.

Anna Money

- Open-amount links: Yes.

- Pricing: Pay-As-You-Go plan gives first £200 incoming payments/month free, then 0.95% per transaction.

- Integrations needed: None.

Monzo Business

- Open-amount links: No. Fixed amount only.

- Pricing: Lite plan free; Pro plan £5/month. 1.29% UK cards, 2.9% international cards.

- Integrations needed: None for payment links, but limited flexibility.

Tide

- Open-amount links: No. Fixed amount only.

- Pricing: £0/month. About 1.5% flat fee per transaction (includes “Pay by Bank”).

- Integrations needed: None for payment links, but not open-amount.

Revolut Business

- Open-amount links: Unclear if natively supported.

- Pricing: £0–£100+/month depending on plan. 1% + 20p for UK cards, higher for international.

- Integrations needed: Possibly required for open-amount functionality.

Starling Bank

- Open-amount links: No native payment link feature.

- Pricing: N/A (requires third-party tools for payment collection).

- Integrations needed: Yes.

High-street Banks (Lloyds, Barclays, HSBC, NatWest, RBS, Santander, etc.)

- Open-amount links: No.

- Payment links: Some offer limited “pay by link” or “Pay by Bank” with strict limits and no reusable link option.

- Integrations needed: Often require external merchant services.

Summary:

GoSolo and Anna Money are currently the only UK business accounts with native, reusable open-amount payment links. GoSolo stands out for its lower fees, no monthly charges, and seamless integration with business banking and invoicing.

Alternatives (Not UK Business Accounts, but Allow Open-amount Links)

If you’re open to using a dedicated payment processor (rather than a business bank account), several global platforms offer open-amount payment links—though with different fee structures and complexity.

Stripe

- Open-amount (“Pay What You Want”) links: Yes, via Stripe Checkout or Payment Links.

- Pricing: 1.4% + 20p per UK card transaction; higher for international cards.

- Integrations needed: Yes—requires a separate Stripe account and some setup.

- Branding/customization: Extensive, but more complex than GoSolo for non-developers.

SumUp

- Open-amount links: Supported.

- Pricing: 1.69% flat fee per transaction.

- Integrations needed: No, works via SumUp app or dashboard.

Square

- Donation links: Work as open-amount payment links.

- Pricing: 1.75% flat fee per transaction.

- Integrations needed: No, works via Square dashboard.

Zettle by PayPal

- Open-amount links: Unclear if natively supported.

- Pricing: 1.75% flat fee per transaction. Weekly payouts.

- Integrations needed: No, works via Zettle dashboard.

Key takeaway:

Stripe and other payment processors offer “pay what you want” functionality—but with higher fees, extra setup steps, and usually without business banking features. GoSolo integrates open-amount payment links directly into your business account, simplifying everything.

Why GoSolo Is the Simplest Route for SMBs and Freelancers

If you’re tired of juggling multiple apps, worrying about hidden charges, or explaining to clients why they can’t just “pay what they want,” GoSolo is built for you.

- No monthly fee for payment links: Open-amount links are included in your free GoSolo business account. No extra charges for access or usage.

- Lowest transaction fees: Interchange++ means you pay the real processing cost, plus a small margin (0.5% + 20p)—usually less than Stripe, Square, or SumUp, especially for smaller transactions.

- Fully integrated: Create, track, and reconcile payments straight from the GoSolo web or mobile app. No need to switch tools or export data.

- Paired with invoices and Tap to Pay: Use open-amount links alongside traditional invoicing and in-person payments for complete flexibility.

- Branding and customization: Add your business name, logo, payment purpose, and notes—so clients always know they’re paying you.

In short:

GoSolo removes the hassle, the hidden fees, and the technical barriers—letting you offer flexible, customer-empowering payment options without complexity.

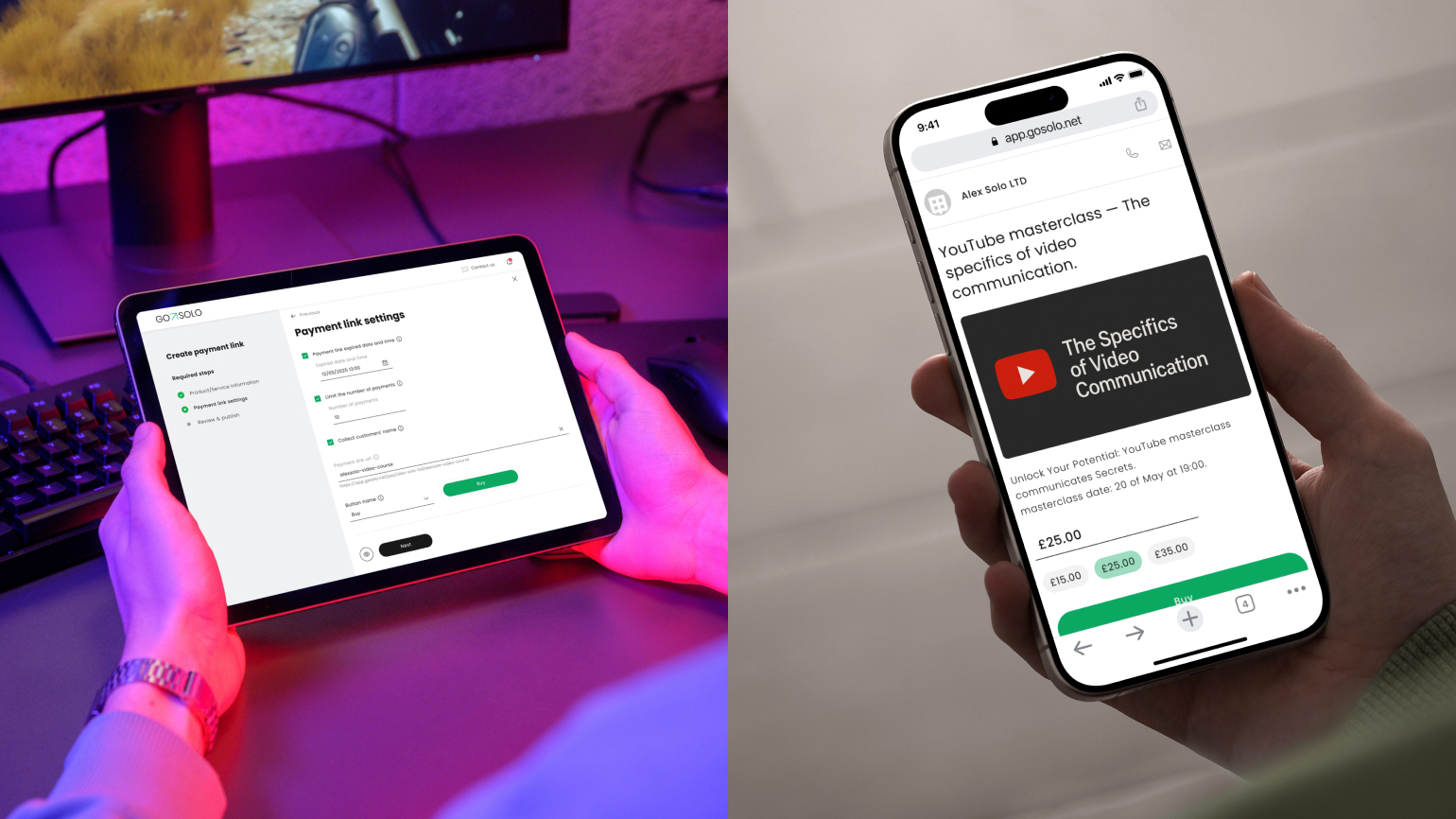

How to Set Up an Open-amount Payment Link in GoSolo

Getting started is refreshingly straightforward. Here’s how it works in practice.

To start off, log in to your GoSolo web dashboard or mobile app.

- Navigate to Sales => Links and click the green Create payment link button.

- Select Clients choose what to pay from the menu.

- Add Product or service information (link name, product/service name, description, and supporting media).

- Set a preset amount or several amounts to guide customers or avoid errors.

- On the next step, you can set an expiration date, payment limits and collect payee's name.

- Choose the button text. You can select between Pay, Buy, Book and Order.

- Preview the checkout page before you proceed.

- Generate the link or QR code and share it via email, SMS, WhatsApp, social media, your website, or even print it out.

- Track payments as they arrive, export transactions for bookkeeping, and match them easily to clients, projects, or invoices.

Pro tip:

You can create as many open-amount links as you need—for different purposes or campaigns. Permanent links can be reused for ongoing collections (like tips, donations, or flexible service fees).

GoSolo Pricing, Limits, Compliance & Risk

Fees and Cost Structure

- GoSolo: Interchange++ (actual card processing cost + 0.5% + 20p per transaction). For most SMBs, this is lower than the 1.4–1.75% flat fees charged by Stripe, Square, or SumUp.

- No monthly or per-link charges. You only pay per successful transaction.

- Other providers: Some have monthly caps, extra fees for high volume, or require paid plans for key features.

Limits and Flexibility

- GoSolo: No arbitrary weekly or per-link caps. Create as many links as you like.

- Other providers: Some restrict number of reusable links, maximum amount per link, or require manual approval for large transactions.

Compliance and Security

- PCI DSS compliance: All card data is processed securely by GoSolo’s payment partners—no sensitive details ever touch your device.

- Fraud prevention: Built-in risk monitoring and alerts; you can set minimum/maximum amounts to reduce accidental or suspicious payments.

FAQs

Is a “pay what you want payment link app” safe?

Yes—when you use a reputable provider like GoSolo, Stripe, or SumUp, all payments are processed securely with full PCI compliance and fraud monitoring. Never share payment links in public spaces unless you’re comfortable with anyone using them.

Do open-amount payment links work with Apple Pay and Google Pay?

Absolutely! GoSolo’s payment links support all major card types, as well as Apple Pay and Google Pay—making it easy for clients to pay from any device.

Can I set a minimum or maximum amount?

Yes. You can specify both a minimum and a maximum amount for each link. This helps prevent accidental underpayment or abuse, while still giving customers flexibility.

Can I reuse the same link for multiple customers?

Yes. GoSolo supports permanent/reusable open-amount links. This is perfect for ongoing collections (like donations or tips), or for situations where you want to share a single payment page with many people.

How is GoSolo different from Stripe’s “pay what you want” feature?

Stripe’s pay-what-you-want payment links are powerful and highly customisable but require a separate Stripe account and more setup. GoSolo integrates open-amount links directly into your business banking—no extra tools, logins, or reconciliation needed. Fees are also typically lower for UK SMBs, and you get built-in invoicing, payment tracking, and account management in one place.